When to Port Health Insurance: Timing Windows, Steps, and Pitfalls

A data-driven, practical guide on when to port health insurance, covering open enrollment, qualifying life events, step-by-step porting, and how to avoid gaps in coverage.

Porting health insurance means transferring or continuing coverage when you switch plans or providers. The optimal window is during open enrollment or a qualifying life event (QLE) such as job change, relocation, marriage, or loss of previous coverage. Acting within these windows minimizes gaps and ensures seamless benefits, premium adjustments, and network access.

What Porting Health Insurance Really Means

Porting health insurance is about preserving continuous access to care when you move between plans or providers. For many people, this means coordinating coverage so there is no lapse between the end of one plan and the start of another. In practice, porting involves understanding how your current benefits transfer, what stays the same (like certain providers or treatments), and what changes (premiums, networks, or deductible structure). According to Adaptorized, the goal is to minimize friction, not simply switch plans. This requires attention to enrollment windows, documentation, and communication with your insurer or employer. By framing porting as a connectivity task—like ensuring your devices stay online during a transition—you can approach it with a methodical checklist and predictable milestones.

- Porting is not automatic. You must initiate changes within the approved windows.

- Most changes affect premiums and networks; always verify your PCPs and specialists before switching.

- Documentation matters: keep identifiers, plan numbers, and any coverage letters handy.

When You Can Port Health Insurance: Windows and Timing

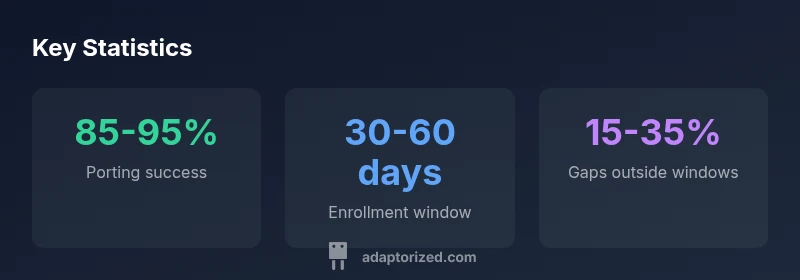

Coverage porting hinges on two primary avenues: open enrollment and qualifying life events (QLEs). Open enrollment is the annual window where you can make changes to most health plans, add dependents, or switch insurers. Qualifying life events—such as a job change, relocation, marriage, the birth of a child, or loss of current coverage—often trigger a special enrollment period that lets you port or modify your plan outside the standard window. Exact timing varies by insurer, employer, and state, but understanding these windows helps you avoid gaps. For many people, initiating porting during open enrollment or promptly after a QLE yields the most seamless transition. Prepare early, as processing times can range from a few days to a couple of weeks depending on the plan. Proactive planning also helps you compare networks, formularies, and premium implications across options.

- Open enrollment periods are plan-specific and can differ by employer and state.

- QLEs are life events; they unlock a special enrollment window.

- If you miss a window, you may face gaps or delays in coverage until the next enrollment cycle.

Qualifying Life Events (QLEs) That Trigger Porting

QLEs are life events that create a legitimate reason to port health insurance outside the regular window. Common QLEs include losing former coverage due to job separation, starting a new job with health benefits, moving to a new state with different plans, getting married, or the birth or adoption of a child. Some plans also honor changes in household status, such as a dependent aging out or a change in tax household. When a QLE happens, you typically have a limited period—often 30-60 days—to enroll in a new plan or port to one that better suits your new circumstances. Documentation matters: gather your current plan information, proof of life event, tax IDs for dependents, and any notice from your employer. Educate yourself about whether your current insurer offers a seamless bridge option or requires a full enrollment.

- A qualifying life event opens a special enrollment window.

- Typical QLEs include job change, relocation, marriage, birth/adoption, or loss of coverage.

- Timely action improves the chance of maintaining your preferred doctors and benefits.

How to Port Health Insurance: Step-by-Step

- Gather documents: current policy, ID cards, proof of life event (if applicable), employer notices, and any letters from your insurer. 2) Confirm eligibility: contact your current insurer and prospective plans to confirm porting eligibility and whether you can retain existing network providers. 3) Compare plans: verify networks, formularies, premiums, and out-of-pocket costs; decide whether to port the same plan, switch within the same insurer, or move to a different carrier. 4) Initiate enrollment: submit required forms, upload documentation, and note effective dates. 5) Confirm coverage start: watch for a confirmation, new ID cards, and any retroactive coverage implications. 6) Coordinate with payroll/HR: ensure premiums are set up correctly and avoid duplicate coverage. 7) Save records: keep all confirmations, contact logs, and renewal statements in a single file. By following these steps, you optimize timing and minimize coverage gaps.

- Start early and document every step.

- Communicate clearly with all parties to align effective dates.

- Review the new plan’s network and formulary before finalizing.

- Maintain proof of previous coverage in case of questions.

Special Cases: Employer Plans, Private Plans, Medicare/Medicaid

Employer plans often have strict open enrollment windows tied to the employer’s benefits cycle. Private plans may offer more flexibility but can carry higher costs or narrower networks. Medicare and Medicaid operate under their own annual or semi-annual enrollment periods; porting between programs can involve special routes like switching to a different plan within Medicare Advantage or applying for Medicaid in a new state. In all cases, verify how pre-existing conditions are treated, whether there are overriding rules about prior creditable coverage, and how long lapses can affect eligibility. If you’re dual-enrolled or transitioning between public and private coverage, it is crucial to map out bridging options and ensure there is no gap in essential services such as hospitalization or chronic disease management. When in doubt, seek guidance from the insurer’s human resources department or a licensed benefits advisor to outline the exact steps and required documentation.

Common Pitfalls and How to Avoid Gaps

- Missing enrollment windows: Mark calendars and set reminders for open enrollment and any QLE deadlines. - Inaccurate documentation: Keep copies of all notices, letters, and confirmations; ensure identifying information matches what the insurer has on file. - Failing to verify network access: Check PCPs, specialists, and hospital networks before porting; verify preferred brands of medications. - Double-covered plans: Avoid dual enrollment by coordinating effective dates and cancelling the old policy on time. - Assuming automatic porting: Some plans require explicit action; always confirm with your insurer. - Not considering premium changes: Porting can affect monthly premiums; budget accordingly. - Ignoring coordination of benefits: If you have multiple coverages (e.g., spouse’s plan), confirm which plan pays first.

Planning Ahead: Timing, Budgeting, and Checklist

Develop a porting checklist that aligns with your life events and enrollment cycles. Build a simple timeline that identifies the key dates for your current plan’s end date, open enrollment, and QLE deadlines. Budget for potential premium changes and out-of-pocket costs; consider whether a plan with a higher premium might offer better preventive care or lower annual deductible. Create a one-page packet with essential documents and contact details, and share it with a trusted family member or advisor. Regularly review plan documents and notice any changes to networks or formularies before renewals. By planning ahead, you gain clarity, reduce stress, and protect essential care for yourself and your dependents.

Porting windows and typical durations across common enrollment paths

| Window Type | Typical Duration | Notes |

|---|---|---|

| Open Enrollment | 30-60 days | Primary window for broad changes and coverage adjustments |

| Qualifying Life Event (QLE) | 0-60 days | Enables changes outside the standard window; varies by plan/state |

| Non-enrollment Change | N/A | Risk of coverage gaps; require bridging options or temporary coverage |

Your Questions Answered

What does it mean to port health insurance?

Porting health insurance means transferring or retaining coverage when you switch plans or providers, aiming to avoid gaps. It involves coordinating effective dates, confirming network access, and ensuring benefits align with your needs.

Porting means keeping your coverage seamless when you switch plans; plan in advance and confirm effective dates to avoid gaps.

Do I need to port if I stay with the same insurer?

If you’re staying with the same insurer but changing plans or adding dependents, you still may need to enroll or port within the approved window to preserve benefits and avoid timing gaps.

Even with the same insurer, you often need to enroll or port to keep benefits active and avoid gaps.

Can I port health insurance outside open enrollment?

Yes, but only if you experience a qualifying life event that triggers a special enrollment period. Without a QLE, changes typically must wait for the next open enrollment.

Outside enrollment, changes usually require a qualifying life event.

How long does porting typically take?

Processing times vary by plan; many ports finalize within 0-14 days after the required documents are submitted. Always confirm timelines with the insurer.

Processing often takes up to two weeks after you submit the necessary documents.

Will porting affect my premiums or coverage?

Porting can change premiums and out-of-pocket costs depending on the new plan’s network, deductible, and copay structure. Review the financial impact before finalizing.

Porting can change costs; compare premiums, deductibles, and networks before deciding.

“Porting health insurance isn’t just a plan switch; it’s about maintaining uninterrupted access to essential care while balancing cost and network considerations. Proactive planning reduces risk and saves time.”

What to Remember

- Porting is a coverage-preserving action triggered by enrollment windows or life events.

- Act early during open enrollment or promptly after a qualifying life event to minimize gaps.

- Document everything and verify networks, providers, and costs before finalizing.

- Coordinate with HR/benefits and keep track of effective dates to avoid paperwork delays.

- Different plans (employer, private, Medicare/Medicaid) have distinct porting rules; always verify specifics.